How to Be a Great Investor, Part Seven: Beware of Behavioral Biases

This article is the seventh in a ten-part series loosely based on Michael J. Mauboussin’s white paper “Thirty Years: Reflections on the Ten Attributes of Great Investors.” See “Part One: Be Numerate,” “Part Two: Understand Value,” “Part Three: Properly Assess Strategy,” “Part Four: Compare Effectively,” “Part Five: Think Probabilistically,” and “Part Six: Update Your Views Effectively” for previous installments. And please keep in mind that although I’m basing my work on Mauboussin’s, I am departing from his ideas on occasion.

Mauboussin writes,

We tend to operate with rules of thumb (heuristics), which are generally correct and save us lots of time. But these heuristics have associated biases that can lead to departures from logic or probability. Examples of heuristics include availability (rely[ing] on information that is available rather than relevant), representativeness (placing people or objects in categories that are inaccurate), and anchoring (placing too much weight on an anchor figure). There is now a long list of heuristics and biases, and great investors are those who not only understand these concepts but take steps to manage or mitigate behavioral biases in their investment process.

Michael J. Mauboussin

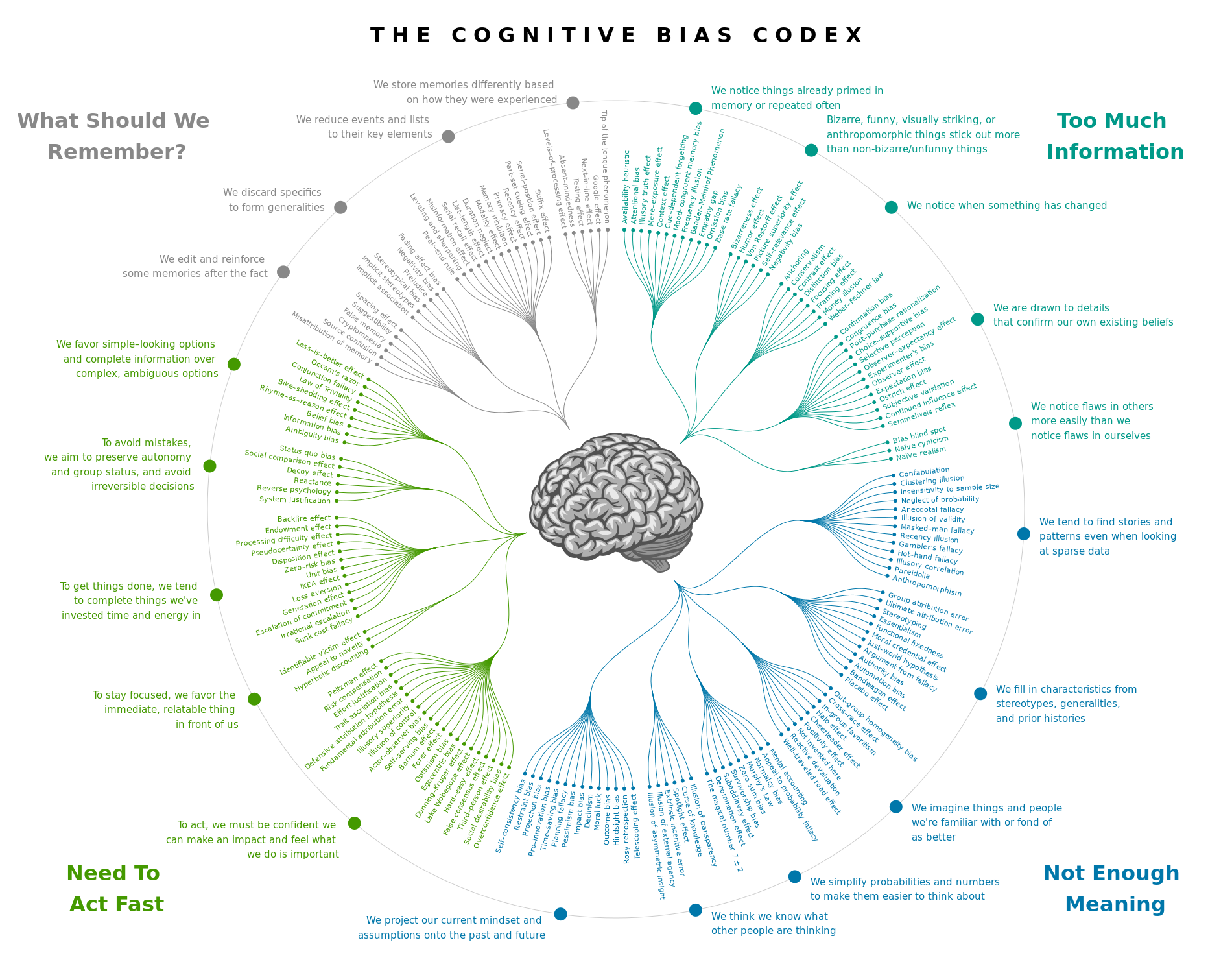

Wikipedia has posted a terrific classification of hundreds of these biases, which is worth looking at. I’m copying it below, but I suggest you go to the link for better readability and to be able to click on the biases.

In this article I’m going to list, in alphabetical order, ten biases that are inimical to being a great investor.

Anchoring

Let’s say two investors buy the same stock. Investor A paid $70 for it and investor B paid $100 for it. The stock is presently worth $85. Investor A will be happy and likely to think favorably of the stock because he made 21% on it; investor B will be sad and likely to think unfavorably of the stock because he lost 15% on it. Both of them will anchor their views about the stock on the price they paid for it. In fact, the value of the stock depends entirely on its prospects and has nothing to do with its past price. Investors A and B should not, if they are perfectly rational, consider for a moment what they paid for it when they decide whether to hold the stock or sell it. (The exception, of course, is if you’re investing in a taxable account, in which case, all else being equal, Investor A might want to keep the stock for at least 365 days and investor B might want to sell it at a loss to offset the profits on other stocks.)

Anecdotal Evidence

When an investor tells you in detail about two or three incredibly successful trades she made and doesn’t tell you about the hundred or so unsuccessful ones, she’s giving you anecdotal evidence. When you justify buying a tiny tech stock because Apple was once a tiny tech stock, you’re relying on anecdotal evidence. When all your friends are buying stuff from Amazon so you’re going to short retail stocks, or you decide to short Chinese stocks because a virus broke out in Wuhan, you’re relying on anecdotal evidence. If you invested in 3D printers or e-cigarette makers because they were new and trendy technologies, you relied on anecdotal evidence. Investment marketing is full of anecdotal evidence: if you had subscribed to such-and-such newsletter, you would have bought Netflix in 2003! (Of course, you’re not told what else you would have bought in 2003.)

Congruence Bias

This refers to the fact that people are much more likely to test a hypothesis by seeing if it works than by trying to disprove it. At the website I use for backtesting (which—full disclosure—also employs me), Portfolio123, there’s a lot more emphasis on making your backtests work well than on trying to make them fail, even though both are essential before you actually implement a system.

Escalation of Commitment (or the Sunk Cost Fallacy)

When an investment thesis is failing, do you pull out your resources and invest in a more promising alternative, or do you double down and hope that persistence will eventually pay off? If the objective evidence suggests that staying the course is unwise, many people will justify their decision to do so nonetheless by invoking the “sunk costs” argument—you’ve already put so much time/effort/money into the project that you can’t just walk away! In fact, the amount of time/effort/money you’ve put into a project often has very little to do with its eventual outcome. If you buy stock in a company and the price of that stock falls by fifty percent, it’s only natural to reassess your decision. But what you should focus on is the company’s prospects at the present moment, not the price you paid for the stock. It’s possible that nothing essential has changed about the company, in which case you should stick to your guns; but if the price fell for a good reason and the company’s prospects are no longer nearly as good as they used to be, and if the price is now more likely to fall further than to rise, it’s best to cut yourself loose, no matter how much you’ve sunk into the investment. The present commitment you have to your investment should be proportional to its prospects, not to your past commitment to it.

Essentialism

This refers to the tendency to assign to every entity an immutable essence. A Ford is a Ford, you might say, and that’s not going to change, even if the company is engaged in a variety of businesses that most people don’t associate with Ford; Coca-Cola is always going to be fundamentally about Coca-Cola, even if the company also owns Costa Coffee and Honest Tea and Minute Maid juice and Smart Water. Some investors will avoid stocks in certain sectors or industries without looking at what separates those stocks from other stocks in those sectors or industries. Others will lump all stocks together as “too risky” without considering that the funds and ETFs they’re investing in are in many cases much riskier than certain low-risk stocks.

The Horns and Halo Effect

In investing, this is the idea that there are some companies that are inherently good or inherently evil; one should invest in those that are good and avoid those that are evil. Gun makers, oil companies, for-profit education companies, and tobacco companies are all tarred with the “evil” brush. In fact, depending on their price, some of these companies will make very good investments, and you’re not tainting yourself by buying their shares on the secondary market since the money you pay for those shares don’t go into these companies’ pockets, and since the money you might make on investing in them can then be used to support your favorite charity or political cause. On the other hand, some very well-intentioned companies are either terrible businesses or are vastly overpriced, and by buying shares in them you’re not helping them in any way. (Of course, this is different if you’re spending millions of dollars on shares in a tiny company, in which case you might elevate or lower the share price by buying or selling.) At any rate, how good or evil a company is should not affect your judgment of its investment potential.

Hyperbolic Discounting

Because all worthwhile investments compound, their net present value is discounted to reflect opportunity costs. In other words, if you have an opportunity to invest at 10%, then the net present value of $1 million in three years is $1,000,000/1.13, or around $750,000, because $750,000 invested at 10% will compound to $1 million in three years. Hyperbolic discounting refers to the familiar tendency of most people to prefer a guaranteed payment of $10 today to $12 tomorrow but to prefer $12 in 101 days to $10 in 100 days. In both cases there’s a one-day difference in payment, but we discount hyperbolically: money in the very near future is worth far, far more than money in the more distant future. Let’s say you have $25,000 to spare and are given the following once-in-a-lifetime choice. You can buy a stock that has a 70% chance to double in price over the next six months and a 30% chance to lose its entire value; or you can buy a zero-coupon bond with a face value of $50,000 that matures in three years (for those who don’t know what a zero-coupon bond is, this basically guarantees that you’ll get $50,000 in three years’ time). Assuming a discount rate of 5% per year, the net present value of the stock is 0.7*50,000/1.05^0.5 = $34,156.50; the net present value of the zero-coupon bond is 50,000/1.05^3 = $43,191.88. Even if the discount rate were 15% to reflect inflated opportunity costs, the zero-coupon bond is still worth slightly more. But many investors, especially young ones, will choose the first option, thus essentially assuming a hyperbolic discount rate of greater than 15%.

Illusions of Control

In 2003, some researchers from business schools in the UK performed tests on over a hundred traders in London investment banks to see how susceptible they were to illusions of control. They found a significant inverse relationship between illusions of control and performance (as measured by their managers and by their remuneration). In other words, traders who assumed that the successes and failures they experienced were entirely due to their own actions performed far worse than those who acknowledged the large role of chance in their performance. The researchers concluded that “illusions of control may cause insensitivity to feedback, impede learning, and predispose toward greater objective risk-taking (since subjective risk will be reduced by illusion of control).” They quote one manager: “It’s very easy when you’re making lots of money to double up and double up and take unnecessary risk. This is just human nature. You think you’ve become slightly God-like and you can actually see a lot more than the market can.”

Recency Effect

This is the proclivity of investors to value recent information more than less recent information. One can document this quite easily by looking at earnings increases. Let’s look at stocks whose earnings have increased over the last four quarters, compared to the previous four quarters, by an average of at least 20%. If you limit yourself to stocks with a market cap over $50 million and look at their performance between 1999 and today, these stocks have an average three-month increase in price of 2.99%, compared to the average three-month increase in all $50-million-or-higher stocks of 2.58%. (I did the testing for this using Portfolio123.) Now let’s compare two subsets of these stocks. One subset had increases in three out of the last four quarters; the other subset had an increase only in the most recent quarter. The first subset has an average three-month return of 3.11%, while the second has a higher average three-month return of 3.17%, illustrating the recency bias quite well. But if you look at their twelve-month returns, it’s entirely different. The first subset has an average twelve-month return of 11.89% while the second has an average twelve-month return of 9.51%. And this is exactly what logic should have told you: that stocks with quarter-to-same-quarter-last-year earnings increases in three or four out of the last four quarters should perform much better than stocks with increases in only one out of the four. But most investors fall prey to the recency effect, and favor stocks with big recent increases over those with steady increases.

Selective Perception

Two investors are monitoring the latest developments in competing companies A and B. Investor A has stock only in company A and investor B has stock in only company B. The latest news features good and bad news about both companies. Investor A is going to weight more heavily the good news about company A and the bad news about company B; investor B is going to do the reverse. If they were perfectly rational, they would ignore the fact that they were shareholders and try to consider the news about the companies fairly.

Other Biases

There are plenty of other behavioral biases that investors succumb to, such as ignoring base rates when making predictions or FOMO (fear of missing out) or the belief that the price of something is what it’s actually worth. Trying to rid oneself of all heuristic biases is a Herculean task, and not even great investors accomplish it completely. But before you make your next major investing decision, it’s a good idea to step back and wonder if a perfectly rational being (if such a thing could exist) would do the same thing.